Several Bajaj Group companies released their Q1 FY26 results, showing strong operational growth. Yet, market sentiment turned cautious, especially for Bajaj Finance, as concerns over asset quality and rising credit costs weighed on the stock.

Let’s break down the recent updates from Bajaj Finance, Bajaj Auto, Bajaj Finserv, and Bajaj Holdings — and what it means for investors.

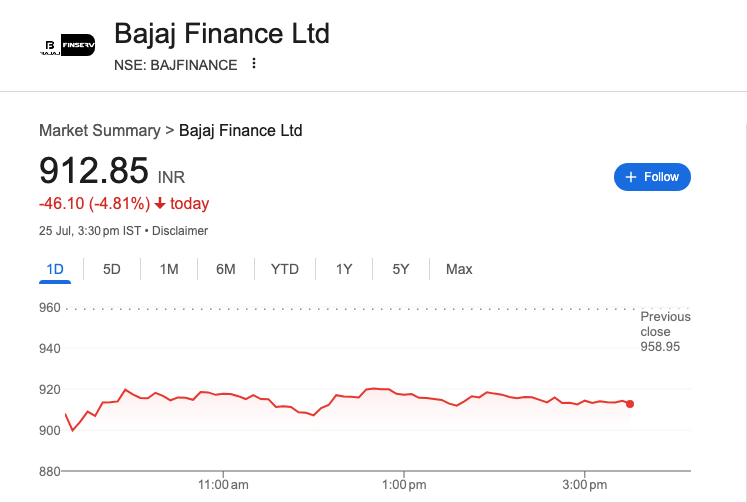

Bajaj Finance Q1 FY26: Strong Profits, But Rising NPAs Trigger Selloff

Financial Highlights

| Metric | Q1 FY26 Value | YoY Change |

|---|---|---|

| Net Profit (Standalone) | ₹4,133 crore | +22% |

| Net Interest Income (NII) | ₹10,227 crore | +22% |

| Assets Under Management (AUM) | ₹3.25 lakh crore | +24% |

| New Customers Added | 4.7 million | – |

| New Loans Booked | 13.5 million | – |

Despite these impressive numbers, the stock fell over 6% on July 25, 2025, opening at ₹906.40 and trading as low as ₹897.65.

Investor Concerns

- Gross NPA rose to 1.28% from 1.06% last year.

- Net NPA increased to 0.63%, up from 0.47%.

- Credit costs surged to 2.02%, above the guided range of 1.85%-1.95%.

- MSME segment stress remains a key risk, with around 12% of the book under pressure.

Analyst Actions

| Brokerage | Rating | Target Price |

|---|---|---|

| UBS | Sell | ₹750 |

| Bernstein | Underperform | ₹640 |

| JPMorgan | Neutral | ₹970 |

| Jefferies | Buy | ₹1,100 |

Bajaj Auto: Steady Exports Offset Domestic Slowdown

June 2025 Sales Breakdown

| Category | June 2025 | YoY Change |

|---|---|---|

| Total Sales | 3,60,806 units | +1% |

| Domestic Sales | 1,88,460 units | -13% |

| Exports | 1,72,346 units | +21% |

| Two-Wheelers | 2,98,484 units | -2% |

| Commercial Vehicles | 62,322 units | +14% |

Exports remain a strong growth area, particularly in the commercial vehicle segment where export growth stood at 49% YoY.

Share Price Snapshot

- Current Price: ₹8,075.50

- Down 2.57% from previous close

- 52-Week Range: ₹7,089.35 – ₹12,774.00

- Market Cap: ₹2.25 lakh crore

Analyst Outlook

- Consensus: Moderate Buy

- Avg. Target Price: ₹9,261 – ₹9,275

- Target Range: ₹7,250 – ₹12,584

Bajaj Finserv: 30% Profit Growth, But Stock Drops

Q1 FY26 Highlights

| Metric | Value | YoY Change |

|---|---|---|

| Consolidated Net Profit | ₹2,789 crore | +30% |

| Total Income | ₹35,451 crore | +13% |

| Interest Income | ₹18,889 crore | +22% |

| Insurance Premium | ₹12,804 crore | +4% |

| Emerging Business Loss | ₹142 crore | As expected |

Despite solid results, Bajaj Finserv shares fell 2.3% to ₹1,985.50, with traders booking profits and reacting cautiously to overall group trends.

Bajaj Holdings: Strategic Moves and Dividend Payouts

Recent Developments

- Sold 0.65% stake in Bajaj Finserv worth ₹2,002 crore.

- Recommended ₹28 final dividend for FY25.

- Scheduled 80th AGM on August 6, 2025.

- Approved acquisition of up to 19.95% stake in both Bajaj Allianz Life and General Insurance companies.

Financial Snapshot

- Stake Holdings: 33.43% in Bajaj Auto, 39.29% in Bajaj Finserv

- Debt-Free for 5 consecutive years

- Maintained a 21.4% dividend payout ratio

Market Challenges

Key Risks to Watch

- Domestic demand slowdown affecting Bajaj Auto’s core sales.

- Asset quality concerns in lending business (MSME and 2-wheeler loans).

- Elevated credit costs affecting margins in Bajaj Finance.

Growth Opportunities

Key Drivers

- Strong export growth, especially in commercial vehicles.

- Premium bike segment (KTM, Triumph) showing traction.

- Electric mobility (Chetak EV) gaining popularity.

- Lending book (AUM) continues to grow steadily.

FAQs

Is Bajaj Finance still a good investment after Q1 results?

While profits are growing, rising NPAs and credit costs have made analysts cautious in the short term. Long-term outlook depends on improving asset quality and loan book performance.

Why did Bajaj Auto’s stock fall despite decent sales?

The fall is largely due to weak domestic sales and overall market volatility. However, export strength remains a positive sign.

What’s driving Bajaj Finserv’s performance?

Robust income from lending and insurance businesses. Losses from new ventures are expected in the early stages.

Is Bajaj Holdings a safe stock?

With a debt-free balance sheet, consistent dividends, and strategic investments, Bajaj Holdings is considered relatively stable among its group peers.

Final Thoughts

Bajaj Group companies are navigating a challenging macro environment with solid financials but visible headwinds in lending and domestic consumption. Investors may need to adopt a selective and long-term approach, especially as exports, digital finance, and EVs continue to shape the group’s next growth phase.